Housing affordability – rather, the lack thereof in Australia has been a salient issue this past decade (pre-COVID too). Heaving heaps of headlines over the years have been celebrating rising prices, bemoaning unaffordability, even fearing a house market crash.

But when did it get so bad? COVID? 2017? Even the early 2000’s? This essay looks at varying factors to try and find when, and maybe even why.

[Liam is studying a Bachelor of Engineering (Honours)/Bachelor of Commerce, majoring in Civil Engineering and Economics. He is interested in macroeconomics and the intersection of politics along the way]

Firstly, a comparison of how house prices have changed over the past few decades.

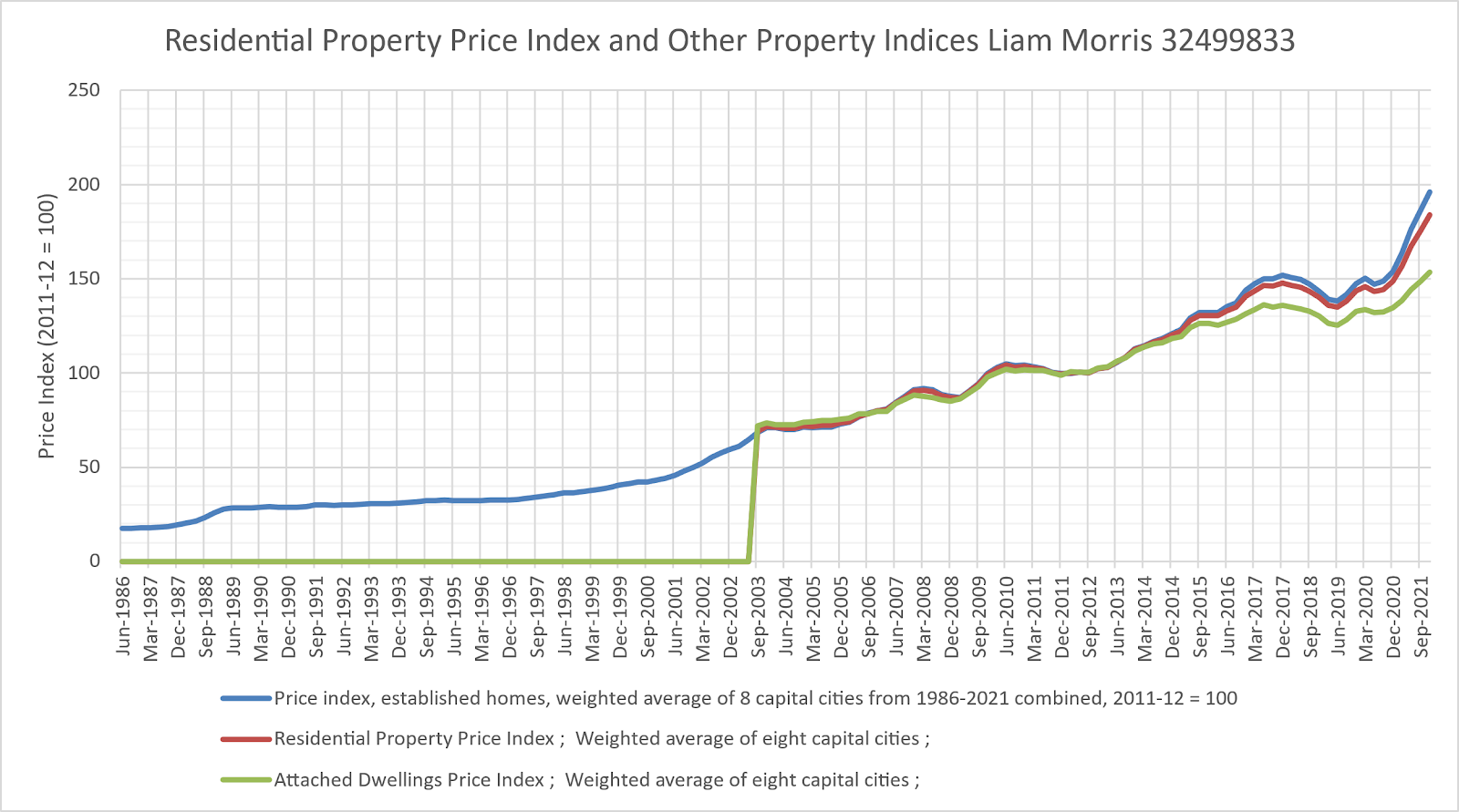

Figure 1: Graph comparing residential property indices with 2011-12=100, using tables 7-8

The above graph (figure 1) is a weighted average of established home prices in all the state capitals plus Canberra and Darwin, which covers around 67% of Australians. A value of 200 would mean a price 2x as high as the baseline year (set to 100) – in this graph, 2011-12. The other indices track fairly closely to each other (and are nearly identical pre 2014), so the established homes index will represent housing as a whole.

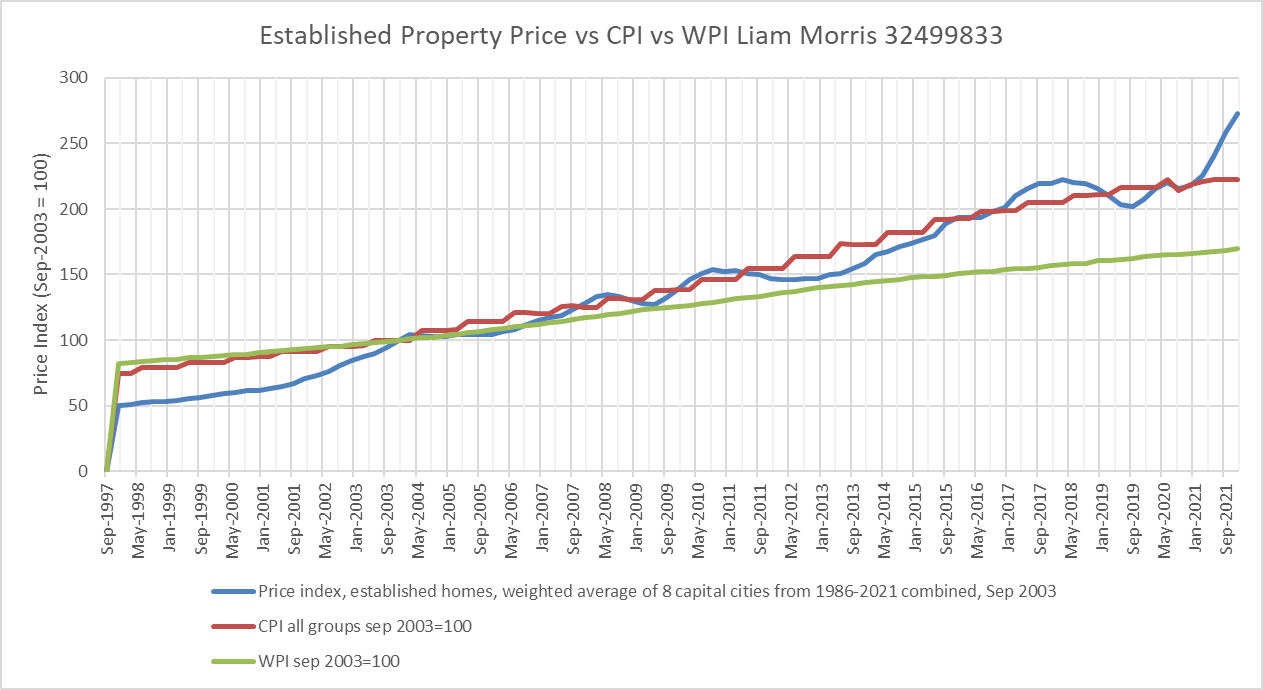

Figure 2: Graph comparing property, CPI, and wages, 1997-2021, with a 2003 baseline.

However, on different metrics, housing unaffordability seems to not be such a longstanding problem.

Graph 2 makes it clear that, for at least 2004 to 2021, house prices didn’t stray too far from CPI, apart from Sep 2011 to Sep 2015. However, for the past two decades, wages have chronically lagged both measures. House prices and the CPI had increased by roughly 2.1 times by the start of 2019 (relative to September 2003), while wages had only increased 1.6 times.

It’s also noteworthy that house prices were lower relative to both consumer prices and wages in the late 1990’s and early 2000’s, suggesting housing affordability is not simply a recent issue.

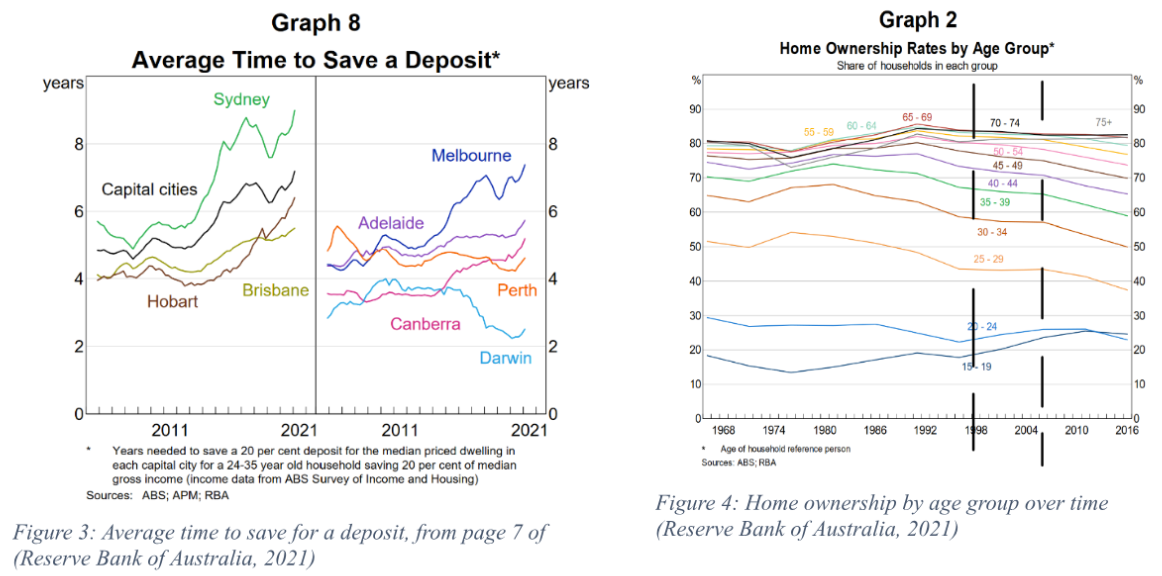

In terms of decreasing affordability, from 2001 to 2021 the average time to save for a deposit rose in all capitals excluding Darwin. Just measuring home ownership directly, as in figure 4, those that are 25-59 years old in 2016 own homes at a lower rate than those in 2004 and earlier.

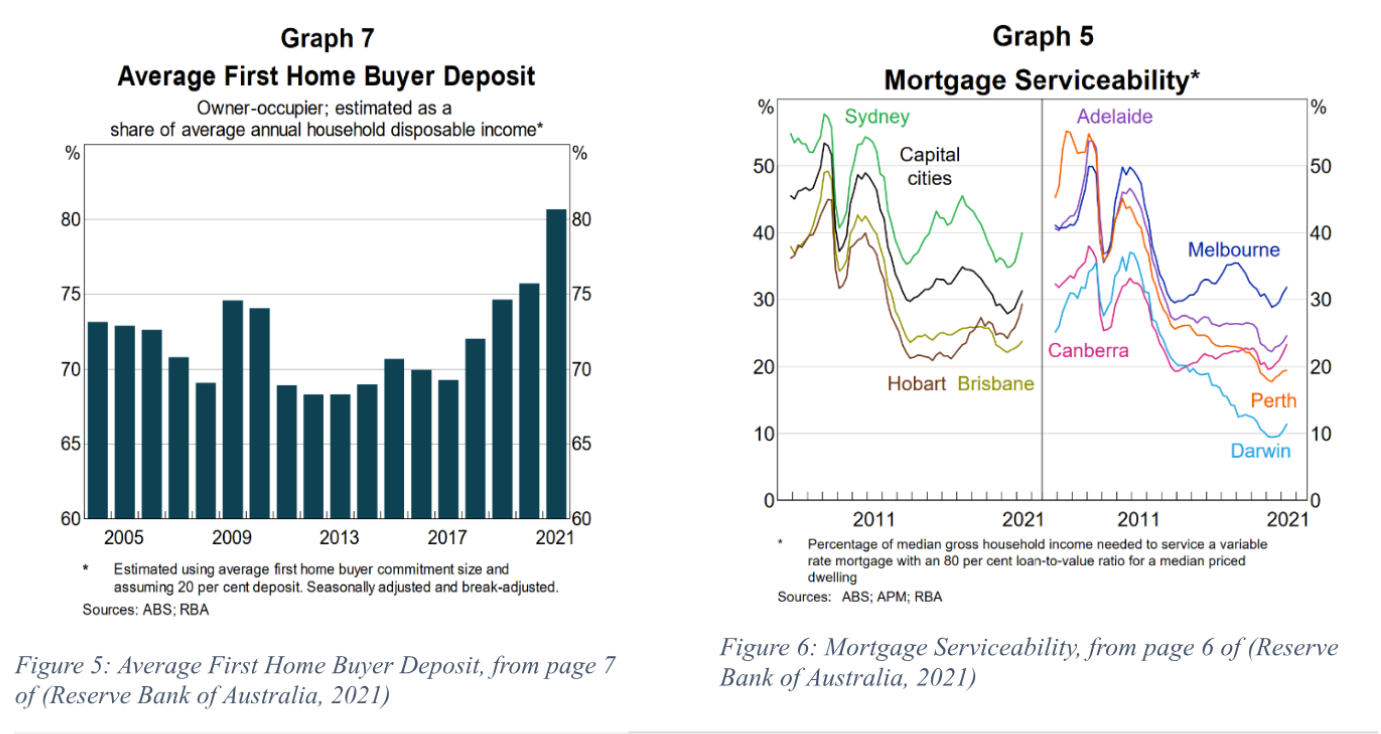

However, on different metrics, housing unaffordability seems to not be such a longstanding problem. First home buyer deposits as a share of income only increased from 2017, staying below 70% from 2008 onwards (figure 5), and mortgage serviceability improved drastically after 2011.

While this may suggest unaffordability is more recent, there are other factors that could account – such as stricter lending limits introduced around 2017, and a drop in the RBA cash rate in 2011 that will be discussed later.

A sudden spike in demand is one of the main reasons that is attributed to housing shortage. If the growth in population is greater than the growth in dwellings, then the equilibrium price where supply meets demand should be higher.

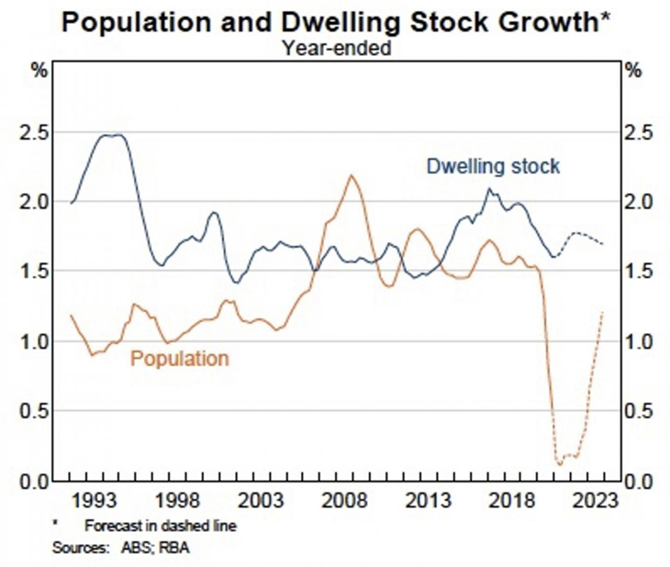

Based on the RBA’s submission to the Senate Economics References committee (figure 7)supply was an issue – at least for most of 2006 to 2015, due to an increase in population growth (international student influx, urbanisation preference). By contrast, all other years (up to COVID) had dwelling stock growing faster than population.

Figure 7: RBA graph of Population and Dwelling growth from 1993 to 2023 (Reserve Bank of Australia, 2021)

Saul Eslake’s submission in 2013 to Parliament (figure 8) also pins supply as the issue, with population growth equal to or greater than housing growth from 2001-2011

Both these suggest, at least for the 2000s, supply would have been an issue, but it is less clear whether a supply shortage would explain high house prices from 2015 to COVID.

Another factor may be low RBA Cash Rates, which mortgage rates often follow. Even after one of the fastest rate rising cycles in recent history, the 4.10% cash rate in September 2023 is still below 2011 levels (~5%, as per Figure 9), and rates from the 1990’s onwards. Low mortgage rates mean homebuyers can afford to service higher prices. The fact that mortgage serviceability improved post 2011 while the average time to save for a deposit increased (shown earlier) reflects this.

Figure 9: RBA cash rate from 1990 to 2023

Finally, another reason could be taxation policy – negative gearing and discounted capital gains tax. Negative gearing allows losses (eg maintenance costs) of running a rental property to be offset against rental income (and also personal income in Australia) to reduce tax. This wouldn’t be a money-spinner by itself as the tax savings wouldn’t be more than the loss (e.g. losing $1 to reduce tax by $0.45 at the top marginal rate) – but it is when capital gains are accounted for.

Capital gains tax (CGT) is the tax on profit made from selling capital i.e. assets – eg shares, or property. This would be added to personal income and taxed like personal income – so if you were in the 45% income tax bracket, any capital gains would be taxed at 45%. Holding an asset for more than 12 months gives a CGT discount, where they tax only half the capital gains – a 50% discount. This would mean what was once taxed at 45% is now taxed at 22.5%. Before the 1999 Howard government changes, this discount was only against gains from inflation. Being able to use losses to offset income taxed at 45%, and only getting taxed on property profit at 22.5% is more profitable, especially when house price rises can far offset rental losses. This allows for investors to buy more property than they otherwise would have, squeezing out first home buyers.

Even with the convenient timing of the 1999 CGT discount changes, however, it may not have a major impact. The Grattan Institute in 2016 found reducing the CGT discount and limiting negative gearing would have, at most, a 2% reduction in house prices in the long run.

In conclusion, house prices jumped relative to inflation from 2000 to 2004, and tracked closely since; but continued to outstrip wages for the past 20 years. Falling mortgage rates offset this (until recently), but underlying affordability is lacking as deposits climb along with house prices.

There was a supply shortfall from 2004 to 2015, but not in 2015 to 2021, which complicates supply as an explanation for prices rises in the latter half of the 2010’s.

References

ABS CPI. (2023, July 26). Consumer Price Index, Australia. Retrieved from Australian Bureau of Statistics: https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/consumer-price-index-australia/latest-release

ABS Residential Property Price Indexes. (2022, March 15). Residential Property Price Indexes: Eight Capital Cities. Retrieved from Australian Bureau of Statistics: https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/residential-property-price-indexes-eight-capital-cities/latest-release#data-downloads

ABS WPI. (2023, August 15). Wage Price Index, Australia. Retrieved from Australian Bureau of Statistics: https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/wage-price-index-australia/latest-release

Eslake, S. (2013, December 21). AUSTRALIAN HOUSING POLICY: 50 YEARS OF FAILURE – Submission to the Senate Economics References Committee. Retrieved from Australian Parliament House: https://www.aph.gov.au/DocumentStore.ashx?id=99cfa3f6-858f-467d-91a9-31e384534a5e&subId=31798

Hutchens, G., & Whitson, R. (2023, May 31). Higher rents will help reduce rental stress by encouraging people to ‘economise’ on housing, RBA governor says. Retrieved from Australian Broadcasting Corporation: https://www.abc.net.au/news/2023-05-31/philip-lowe-says-higher-interest-rates-will-bring-rents-down/102414220

Janda, M. (2021, November 16). Housing affordability won’t be greatly improved just by less regulation, more supply, RBA argues. Retrieved from Australian Broadcasting Corporation: https://www.abc.net.au/news/2021-11-16/housing-affordability-inquiry-rba-evidence/100621256

Maguire, D., & Janda, M. (2024, April 2). What is negative gearing? Why is it so controversial? How does capital gains tax come into it? Retrieved from ABC News: https://www.abc.net.au/news/2024-04-02/what-is-negative-gearing-why-is-it-controversial/103489372

Mares, P. (2021, September 24). Asking the wrong questions about housing. Retrieved from Inside Story: https://insidestory.org.au/asking-the-wrong-questions-about-housing-mares/

Michael Janda. (2017, July 03). Housing surplus raises real estate crash risks. Retrieved from ABC News: https://www.abc.net.au/news/2017-07-03/housing-surplus-raises-price-crash-risks/8663860

Morton, R. (2023, July 13). How to solve the housing crisis. Retrieved from The Saturday Paper: https://www.thesaturdaypaper.com.au/opinion/video/2023/07/13/how-solve-the-housing-crisis

RBA Cash Rate Target. (2023, September 06). Cash Rate Target. Retrieved from Reserve Bank of Australia: https://www.rba.gov.au/statistics/cash-rate/

Reserve Bank of Australia. (2021, September). Submission to the Inquiry into Housing. Retrieved from Australian Parliament House: https://www.aph.gov.au/DocumentStore.ashx?id=8afc3d2d-782f-4fc0-a513-fc15ac572108&subId=713990

Wood, D., & Daley, J. (2016, April). Hot Property: negative gearing and capital gains tax reform. Retrieved from Grattan Institute: https://grattan.edu.au/wp-content/uploads/2016/04/872-Hot-Property.pdf