In a startling move, ASIC has announced it will be suing AustralianSuper over delays that have left thousands of grieving families in limbo. Allegedly, many death benefit claims have been left unprocessed for years, causing families to wait up to four years for a payout. In the last six months, ASIC has ramped up its scrutiny of the superannuation sector by launching similar lawsuits against other superfund giants. As the pattern of deficiencies grows, the question looms: is Australia’s superannuation system capable of upholding its intent, or is it time for a fundamental overhaul?

[Grace Zhou is a fourth year Law and Commerce student outside her role as a Writer at ESSA. Grace has a strong passion for exploring the intersection between macroeconomic policy and the law. She is fascinated by the role of regulatory frameworks such as antitrust law on shaping market efficiency, corporate governance and macroeconomic stability. Combining her analytical skills and an understanding of macroeconomic theory, Grace aims to provide digestible insights to students who wish to learn more about current economic trends, and how regulatory policies shape Australia’s economic resilience and drive sustainable growth.]

Super In the News

In a significant legal development in March this year, Australian Securities and Investments Commission (ASIC) initiated court proceedings against AustralianSuper, trustee of the nation’s largest superannuation fund. ASIC alleges that AustralianSuper has contravened s 912A(1)(a) of the Corporations Act 2001 (Cth) and s 34(1) of the Superannuation Industry (Supervision) Act 1993 (Cth) to conduct its licensed financial services efficiently, honestly and fairly.

Currently, AustralianSuper controls an enormous $367 billion in assets on behalf of 3.51 million members (AustralianSuper, 2025). The legal action pertains to excessive delays in processing 7,000 death benefit claims filed by families of deceased fund members between 2019 and 2024. Affected claims have allegedly taken between four months and four years to be assessed despite all necessary documentation being provided. Regrettably, AustralianSuper is not an isolated case. In November last year, ASIC also blasted civil proceedings against United Super (CBUS Super), accusing the fund of mishandling an estimated total of $20 million relating to death benefit claims and total and permanent disability (TPD) insurance claims (ASIC, 2024).

Problems in Super: Forecasted Underspending

For many of us in the early stages of our careers, we are likely engaging with our super on autopilot. Apart from nominating a fund when we first start work, super savings are contributed unwittingly for the next few decades before most people become acquainted with its implications much further down the line. As such, it may come as a surprise to learn that Australia’s compulsory superannuation system is valued at over $4.2 trillion in assets at the end of the December 2024 quarter (ASFA, 2024). The system is designed to increase retirement security for Australians by promoting self-funded retirement savings and reducing reliance on our public funded pension system. By the early 2040s, the Grattan Institute forecasts that the average Australian retiree will hold a superannuation balance of at least $250,000 in today’s dollars, with the amount reaching nearly $500,000 by 2026 due to projected growth rates (Coates et al., 2025), (see Figure 1.1).

Despite this optimistic forecast, the reality of retirement for most Australians is not as rosy. Research indicates that half of all retirees withdraw only the statutory minimum from their super funds, leaving an astonishing 65% of their super balances untouched by the time they reach the average life expectancy (Coates et al., 2025). This trend seemingly contradicts the design of the compulsory super regime in the first place, which is to counteract people’s biases to under-save for retirement. A key driver for this emerging phenomenon is the fear of retirees to outlive their savings. Retirees battle many uncertainties surrounding their life expectancy, potential health costs, and future aged care needs. In the Intergenerational Report released in 2023, average life expectancy is projected to rise to 87.0 years for men and 89.5 years for women by 2062-63 (Australian Government, 2023), which may further prompt retirees to be more frugal than needed. While Australians over the age of 67 are eligible for the age pension, its reliance on means testing—based on both income and assets—elevates the level of unpredictability that further complicates retirement spending.

Superannuation as an Inheritance Asset

The 2020 Retirement Income Review projected that by 2059, one in every three dollars paid out from the superannuation system will be in the form of death benefits, up from one in five today (Callaghan et al., 2020).

As we continue to see funds being passed down as inheritance rather than being spent during retirement as intended, this raises an array of economic implications. Firstly, Australia is at a critical juncture with its aging population. Currently, one in six Australians are now aged 65 or older (Walsh, 2024). It is forecasted that by 2062, nearly one-in-five Australians will be a retiree compared to less than one in ten today (Grattan, 2025). This demographic shift is set to place immense pressure on Australia’s welfare systems. A growing retiree population will have greater demand for welfare payments and other services relating to the age pension, disability support, social housing and homelessness services. Additionally, indirect pressures will surge to address the accessibility of these services, affecting additional resourcing, infrastructure and personnel to support an expanding cohort of older Australians.

In addition, inflation risk remains a persistent concern. The purchasing power of retirees’ superannuation savings may erode if left unspent or converted into death benefits rather than utilised for retirement needs. This is especially concerning if death benefit payouts continue to be delayed per ASIC’s allegations. Funds that could have been redirected into investment in an attempt to outpace inflation will be missed opportunities for beneficiaries, leaving the next generation with a real value significantly lower than what is anticipated. Moreover, adult children who are considered non-tax dependent beneficiaries of a super member will need to consider added tax liabilities. Despite Australia’s death and probate duty being abolished in 1983, the non-dependency death benefit (NDDB) tax is still a de facto death duty payable by adult children and poses as a significant financial strain on heirs. This will be payable on top of any other de facto death duties, namely the deceased’s assessable stamp duty, income tax and CGT tax. The NDDB tax is incurred at a minimum of 15% plus the Medicare Levy unless a superannuation testamentary trust is in place (Davies, 2017).

Food For Thought

In light of the mounting challenges and legal issues facing Australia’s superannuation system, it is clear that the current framework is struggling to deliver on its primary goal—providing financial security in retirement. As Australia faces increasing demographic and economic pressures, reform may be needed to encourage spending in retirement, thereby mitigating the rising trend of superannuation bequests.

Firstly, the retirement income sector needs to provide workers and retirees with the support, advice and education necessary to break down the complexities of retirement planning. Research shows that only 51% of adult Australians, including around 60% of those aged 65+, have consulted any source of information on preparing for retirement (ASFA, 2024). Additionally, there is a widening gap between financial guidance received by workers and those in the retirement phase about their supers (Grattan Institute, 2025) (see Figure 1.2).

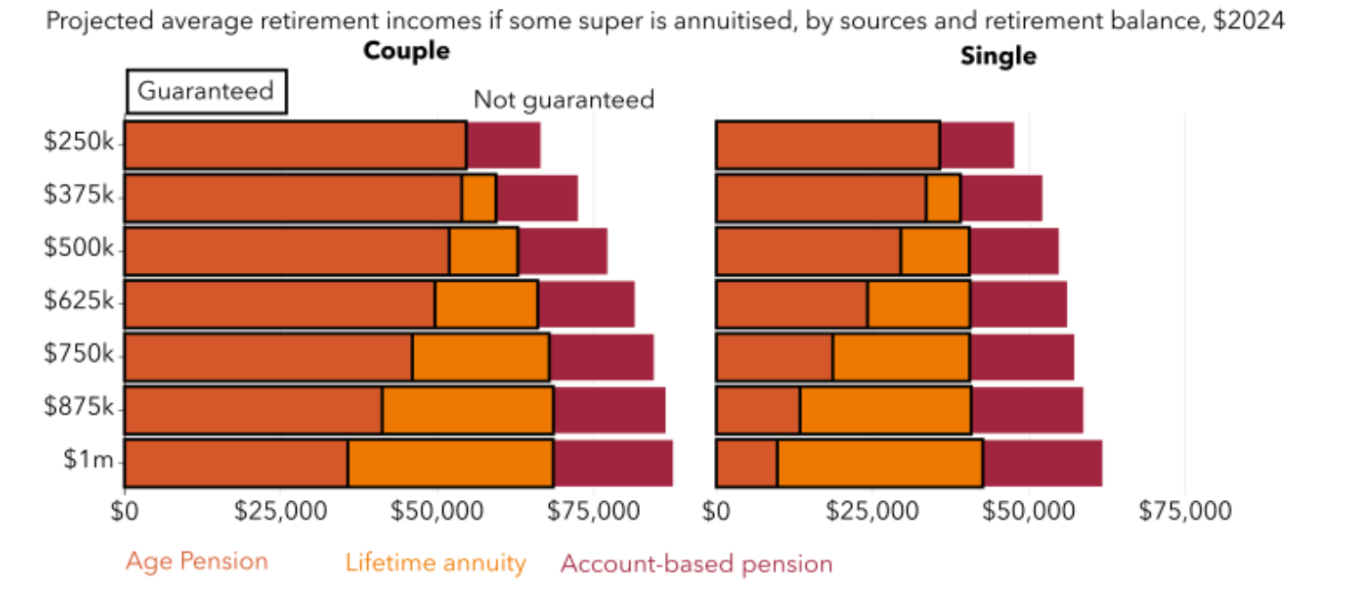

Secondly, is there a possibility of converting superannuation into an annuity or income guarantee for retirees in a way feasible for Australia? This concept mirrors the lifetime income models implemented in countries such as the Netherlands and Sweden (Nuveen, 2024). In these places, retirees are assured a steady income stream regardless of the volatility of investment returns. For Australian retirees above a threshold of $250k in their super balances, purchasing an annuity could boost expected retirement incomes by up to 25% (Grattan Institute, 2024) compared to solely drawing on an account-based pension at legislated minimum rates (see Figure 1.3).

Another potential avenue for reform involves incentivising higher superannuation contributions by employers, although viewed as controversial. Current income tax incentives already favour superannuation savings, therefore some argue that further increasing the minimum SG rates can potentially boost retirement balances and generate greater confidence to spend post retirement.

In conclusion – clearer guidance, more accessible financial planning tools, and policy changes that encourage retirees to spend are essential steps toward ensuring the system’s future sustainability. When considering bridging the gap, the question is no longer whether we can afford to reform the system, but rather, can we afford not to?

References

ASFA. (2024). Super Statistics. Association of Superannuation Funds of Australia. https://www.superannuation.asn.au/resources/super-stats/

About Us, AustralianSuper. (2025). Www.australiansuper.com. https://www.australiansuper.com/about-us

Annuities would take the stress out of retirement – Grattan Institute. (2025, February 3). Grattan Institute. https://grattan.edu.au/news/annuities-would-take-the-stress-out-of-retirement/

ASIC sues Cbus alleging systemic claims handling failures | ASIC. (2024). Asic.gov.au. https://asic.gov.au/about-asic/news-centre/find-a-media-release/2024-releases/24-251mr-asic-sues-cbus-alleging-systemic-claims-handling-failures/

Callaghan, M., Ralston, D., & Kay, C. (2020). Retirement Income Review [Review of Retirement Income Review ]. In Treasury.gov.au (pp. 1–648). Commonwealth of Australia 2020. https://treasury.gov.au/publication/p2020-100554

Chalmers, J. (2023). 2023 Intergenerational Report (pp. 1–296) [Review of 2023 Intergenerational Report]. Commonwealth of Australia 2023. https://treasury.gov.au/publication/2023-intergenerational-report

Coates, B., Moloney, J., & Suckling, E. (2025). Simpler super: taking the stress out of retirement (pp. 1–61) [Review of Simpler super: taking the stress out of retirement]. Grattan Institute 2025. https://grattan.edu.au/wp-content/uploads/2025/01/Simpler-Super-Grattan-Institute-Report.pdf

Davies, B. (2017, January 16). Superannuation Death Tax – 17% or 32% tax for adult children when parents die. Legal Consolidated Barristers & Solicitors. https://legalconsolidated.com.au/super-death-tax/

Nuveen. (2024, November 24). Lessons for retirement systems: Insights from global practices [Review of Lessons for retirement systems: Insights from global practices]. Nuveen, a TIAA Company. https://www.nuveen.com/global/about-us/our-clients/defined-contribution/lessons-for-retirement-systems-insights-from-global-practices

One in two Australians have never accessed information on preparing for retirement. (2024, October 21). ASFA. https://www.superannuation.asn.au/media-release/one-in-two-australians-have-never-accessed-information-on-preparing-for-retirement/

Walsh, E. (2024, October 14). The carer crisis: Why Australia’s ageing population requires employer action. Women’s Agenda. https://womensagenda.com.au/latest/the-carer-crisis-why-australias-aging-population-requires-employer-action/