Why Australia’s energy-shock inflation debate is only the surface of a deeper monetary policy challenge across the Pacific.

Branesh Prakash

ESSA Monash Clayton

[Bran is a Master of Applied Econometrics student at Monash University and an economist with the Reserve Bank of Fiji, currently on study leave as an Australia Awards scholar. His work sits at the intersection of macroeconomics, policy analysis and applied econometrics, with a particular focus on monetary policy and the economic challenges facing small island developing states. This piece reflects his broader interest in bringing a Pacific perspective to Australian economic debates and making technical economic issues and policy practice more accessible to students and the wider public.]

Disclaimer: The views expressed in this article are those of the author and do not necessarily reflect the views of affiliated organisations.

The monetary policy challenge

Monetary policy is often taught as if central banks are steering in calm waters: inflation rises, interest rates respond, and the economy gradually returns to target. But across Oceania, the tides are rarely so still.

The recent conflict in the Middle East has complicated the Reserve Bank of Australia’s (RBA) decision-making surrounding monetary policy. In economic terms, this is a classic negative supply shock: the price of a key input rises, pushing inflation higher while simultaneously weighing on real incomes, consumption and output. For central banks, this creates an uncomfortable trade-off. Higher interest rates may help prevent inflation expectations from drifting upwards, but they cannot address the root cause of the shock: costlier energy prices and disrupted global supply chains.

Australia entered this shock with inflation already above target due to capacity pressures and a somewhat tight labour market (RBA, 2026a). Now, the conflict has driven sharp increases in commodity prices, particularly energy. In May, the RBA delivered a third consecutive rate hike, lifting the cash rate target—its primary monetary policy instrument—to 4.35%, citing higher conflict-induced inflationary risks. The RBA still expects inflation to ease towards the midpoint of the 2-3% target range by mid-2028, but with higher inflation in the near term and greater uncertainty (RBA, 2026b).

This is where textbook rules begin to blur. If inflation is being driven by strong demand, higher interest rates are a natural response that cools spending and brings inflation back down. But when inflation is driven by imported energy prices, monetary policy faces a sharper dilemma. Whether raising interest rates is an optimal response to these conflict-induced challenges in Australia is presently a matter of policy debate.

Look through, or lean against?

The International Monetary Fund (IMF) (2026) acknowledges that the standard policy response to surging global energy prices is to look through it—provided inflation expectations remain well-anchored, and the existing monetary policy stance is appropriately calibrated. This recognises the role of prices as signals: higher prices curb demand or promote supply. In Australia, however, the RBA’s concern is that the shock has arrived while inflation is already above target and capacity pressures remain elevated. While higher fuel prices may first appear in petrol prices, they can gradually pass through to transport, production and distribution costs, lifting prices in the economy more broadly via second-round inflation effects. Importantly, if households and firms begin to expect higher inflation to persist, this can influence wage bargaining and price-setting behaviour. The RBA notes that short-term inflation expectations have already risen since the conflict began. Preventing a temporary supply shock from becoming a more persistent inflation problem underpins the rationale behind leaning against the shock.

On the other hand, Chowdhury (2026) critiques that central banks suffer from inflation phobia and incorrectly weight the risk of destabilising inflation expectations and wage-price spirals. This prompts policy over-reaction via excessive monetary policy tightening, and represses growth unnecessarily. At the same time, interest rate is a blunt tool that may discourage business investments needed for building productive capacity in the economy. Thomson (2026) argues that monetary tightening could have uneven distributional effects in Australia. Asset-rich households may continue spending despite higher rates and prices, leaving poorer households to bear the adjustment needed to reduce aggregate demand. Interestingly, Zhou (2026) models Australian energy shocks and finds that temporary monetary policy easing can improve welfare with little inflation effect during highly volatile geopolitical energy shocks.

Australia’s current debate already shows how quickly monetary policy becomes more complicated. For Pacific Island countries, these complications are not occasional disruptions; they are recurring features of the policy environment.

When external shocks are the norm

Across the Pacific, inflation often arrives from sources external to the domestic economic and monetary system, for instance, imported fuel and food prices, freight costs, exchange rates and natural disasters (Bai et al., 2016). For many Pacific Island countries (PICs), monetary policy is not simply a matter of whether interest rates should rise or fall. Policymakers need to consider how to manage imported inflation while also protecting external stability.

Due to characteristics such as ‘smallness’, remoteness in location and narrow production bases with capacity constraints, PICs tend to heavily depend on imports for consumption and intermediate inputs and on good or service exports, remittances and/or foreign direct investment for income or financing needs. Consequently, they are more exposed to external shocks. Furthermore, as developing economies, food and fuel represent a high share of household consumption baskets. These conditions help explain why PICs often operate under different monetary policy frameworks compared to Australia, and why managing inflation in PICs through monetary policy can be more complex.

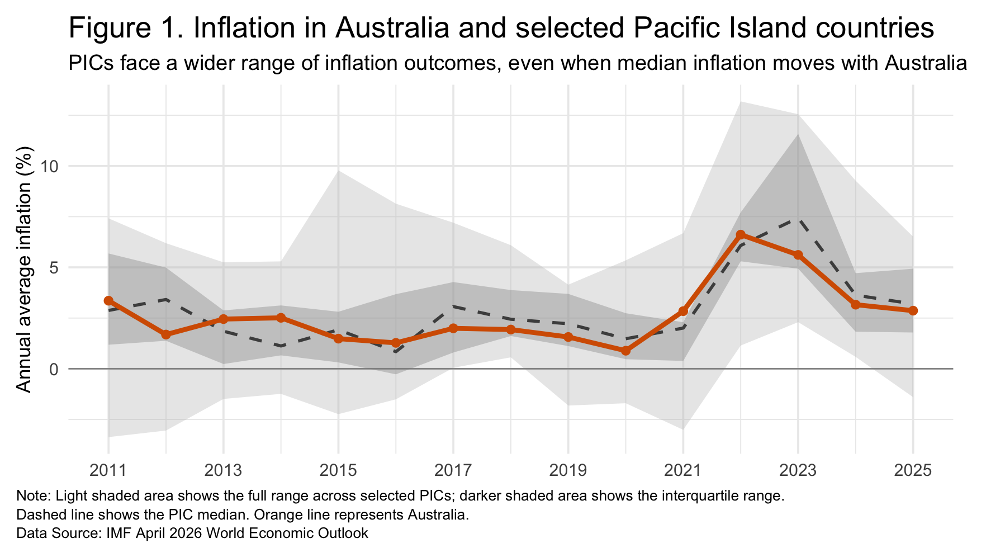

Figure 1 shows the annual average inflation rate by year for Australia (orange) relative to eleven PICs1 (grey shaded regions and black dotted median). The median inflation experience across these PICs moves broadly with Australia, potentially highlighting exposure to similar global price shocks and PICs’ close regional trade link to Australia. The wider shaded bands reflect a more important characteristic—inflation outcomes across the Pacific are more dispersed. For Pacific policymakers, this may imply that the same external shock can be manageable in one country but destabilising in another, depending on foreign reserves, fiscal space, import dependence and the exchange-rate regime.

Beyond the cash rate: monetary policy in small island economies

Understanding policy decisions that PICs need to make requires examining the policy frameworks through which PICs respond to shocks. Australia operates a floating exchange rate and inflation-targeting framework, whereas PICs have diverse monetary arrangements, owing to their structural differences. Some have their own currencies and central banks, while others use the Australian, New Zealand or United States dollar. Even among those with independent currencies, fixed or managed exchange-rate regimes often play a central role in anchoring prices and maintaining external stability.

This matters because, under a fixed or managed exchange-rate regime, monetary policy is not only about stabilising domestic inflation. It is also about maintaining confidence in the currency, which is usually attained by protecting foreign reserves to ensure the economy can continue paying for essential imports on an ongoing basis and during shocks (Yang et al., 2016). In this setting, a global commodity price shock is not only an inflation shock, but a balance-of-payments shock as well. When import bills rise, foreign reserves fall and may come under pressure, making the prevailing exchange-rate arrangement difficult to maintain.

On top of this, the standard interest-rate channel of monetary policy is weaker in PICs than in Australia, which constrains monetary policy effectiveness (Yang et al., 2016). In Australia, changes in the cash rate flow through relatively deep mortgage, deposit and credit markets. In many PICs, shallow financial markets, excess liquidity, high collateral requirements and limited bankable projects weaken the link between policy rates, lending rates and private credit, thereby limiting the pass-through of monetary policy to offset shocks (Wood, 2010). World Bank (2026) observes that despite ample liquidity and low policy rates, private credit growth remains subdued in Fiji and Solomon Islands, while excess liquidity continues to challenge transmission in Samoa and Tonga.

These constraints lead to the classic monetary policy trilemma: a country cannot simultaneously maintain (1) a fixed exchange rate, (2) free capital mobility and (3) full monetary policy independence. A country chooses two goals while giving up the third. For PICs, the triangle is surrounded by a fourth policy dimension, foreign reserves, implying that PICs face a quadrilemma (Su et al., 2018). Central banks in PICs do not simply calibrate policy to inflation and output—as one sees in standard Phillips curve models and Taylor rules—but they also aim to guard the external anchor that allows the economy to import fuel, food and other essentials. With fixed exchange rates, PICs that conduct monetary policy independently implement some level of capital controls and calibrate monetary policy to ensure foreign reserves are adequate. In this space, fiscal policy becomes relevant and requires coordination with monetary policy. For instance, targeted fiscal support can help protect particularly vulnerable households from imported price shocks but must preserve external stability by not unnecessarily stimulating demand, which would build domestic inflationary pressures and weaken foreign reserves via imports.

| Case study: When the exchange rate becomes macro policy—Fiji’s 2009 devaluation Fiji offers a case study to demonstrate how monetary policy in PICs operates differently from Australia’s framework. The Fijian dollar is pegged to a basket of trading-partner currencies, and since Fiji is highly import-dependent, holding adequate foreign reserves to maintain exchange-rate stability is a key part of its monetary policy framework. Fiji’s 2009 devaluation was a policy response to external shocks, which carried adverse consequences on output, inflation and external stability. The global financial crisis had weakened tourism, remittances and export earnings, while earlier global food and fuel price increases had contributed to import pressures and inflation. As reserves fell to critically low levels, Fiji devalued its dollar by 20%, tightened foreign-exchange controls and applied import restrictions (Wood, 2010). This was not a painless policy choice since devaluation raises the domestic price of consumption and intermediate imports, placing further pressure on households and firms. However, relying only on monetary tightening would have been costlier, as weak transmission would have required interest rate rises large enough to lower domestic price levels to an extent needed to rebuild external competitiveness and reserves, and this process would have contributed to a relatively higher loss in output (Yang et al., 2016). In this setting, exchange-rate policy became a macroeconomic stabilisation tool by being more direct than interest-rate policy in addressing external imbalance, but still carrying inflation and distributional costs. The lesson here is not that devaluation is always desirable. Rather, Fiji’s experience shows that the policy environment in small open economies with fixed exchange rates can become quite complex. |

Navigating divergent tides today

In Australia today, the debate centres on whether conflict-induced higher global commodity prices require higher interest rates to prevent second-round inflation effects and protect inflation expectations from drifting upwards. In PICs, this inflation shock also tests the external position. The appropriate response depends on the country’s reserves, fiscal space, exchange-rate regime, inflation expectations and the strength of monetary transmission. Where reserves are comfortable and demand pressures are weak, policymakers may have more room to let global prices pass through while protecting vulnerable households through targeted fiscal support. Where reserves are falling, or confidence in the exchange-rate arrangement is under pressure, the policy response may need to be tighter and broader, involving liquidity management, fiscal restraint, external financing or capital controls, exchange-rate adjustment, or some combination of these.

Conclusion: reading the tides

Oceania shows that monetary policy is less mechanical than what standard models in textbooks suggest. Australia’s current debate highlights the difficulty of responding to inflation when the source is a global energy price shock rather than simply excess domestic demand. But across the Pacific, this challenge is wider and more recurrent: inflation arrives through various sources, and policy must also protect reserves, exchange-rate credibility and vulnerable households. This does not make textbook frameworks irrelevant; it makes them incomplete without context. Ultimately, the appropriate response is a function of various factors, and for me, this is what makes monetary policy so fascinating. It is not just about applying a rule, but about reading the tides appropriately and choosing the least costly path through them.

References

Bai, X., Tumbarello, P., & Wu, Y. (2016). Drivers of inflation in the Pacific Island countries. In: Khor. H. E., Kronenberg, R. P., & Tumbarello, P. (Eds.), Resilience and growth in the small states of the Pacific (pp. 151–162). International Monetary Fund.

Chowdhury, A. (2026, May 7). ‘War-shock inflation’: Reserve Bank’s inflation phobia, no lesson learnt. Centre for Future Work. https://futurework.org.au/news/war-shock-inflation-reserve-banks-inflation-phobia-no-lesson-learnt/

International Monetary Fund. (2026). World Economic Outlook: Global economy in the shadow of war. International Monetary Fund.

Reserve Bank of Australia. (2026a). Statement by the Monetary Policy Board: Monetary Policy Decision. (No. 2026-12). Reserve Bank of Australia.

Reserve Bank of Australia. (2026b). Statement on Monetary Policy: May 2026. Reserve Bank of Australia.

Su, J., Cocker, L., Delana, D., & Sharma, P. (2018). A First Look at the Trilemma Vis- a-Vis Quadrilemma Monetary Policy Stance in a Pacific Island Country Context. Review of Pacific Basin Financial Markets and Policies, 21(1), 1-22, https://doi.org10.1142/S0219091518500029

Thomson, J. (2026, May 9). The RBA’s Problem. Australian Financial Review. https://www.afr.com/politics/federal/the-rba-s-problem-is-we-re-all-too-rich-20260507-p5zura

Wood, R. (2010). Monetary and exchange rate policy issues in Pacific island countries. (Treasury Working Paper No. 2010-05). The Treasury. https://treasury.gov.au/sites/default/files/2019-03/Tsy_Working_Paper_10_05.pdf

World Bank. (2026). Pacific Economic Update. Pacific Jobs Pathway. Special Focus: Water as an Essential Foundation for Jobs. World Bank.

Yang, Y., Davies, M., Wang, S., Dunn, J. & Wu, Y. (2016). Monetary Policy Transmission Mechanisms in Pacific Island Countries. In: Khor. H. E., Kronenberg, R. P., & Tumbarello, P. (Eds.), Resilience and growth in the small states of the Pacific (pp. 229–248). International Monetary Fund.

Zhou, L. (2026). Rethinking monetary policy under global energy price fluctuations: Insights from Australia. Global Economics Research, 2(1), 1-12, https://doi.org/10.1016/j.ecores.2026.100033

Endnotes:

- These include Fiji, Kiribati, Marshall Islands, Nauru, Palau, Papua New Guinea, Samoa, Solomon Islands, Tonga, Tuvalu, and Vanuatu, which are selected based on data availability. ↩︎